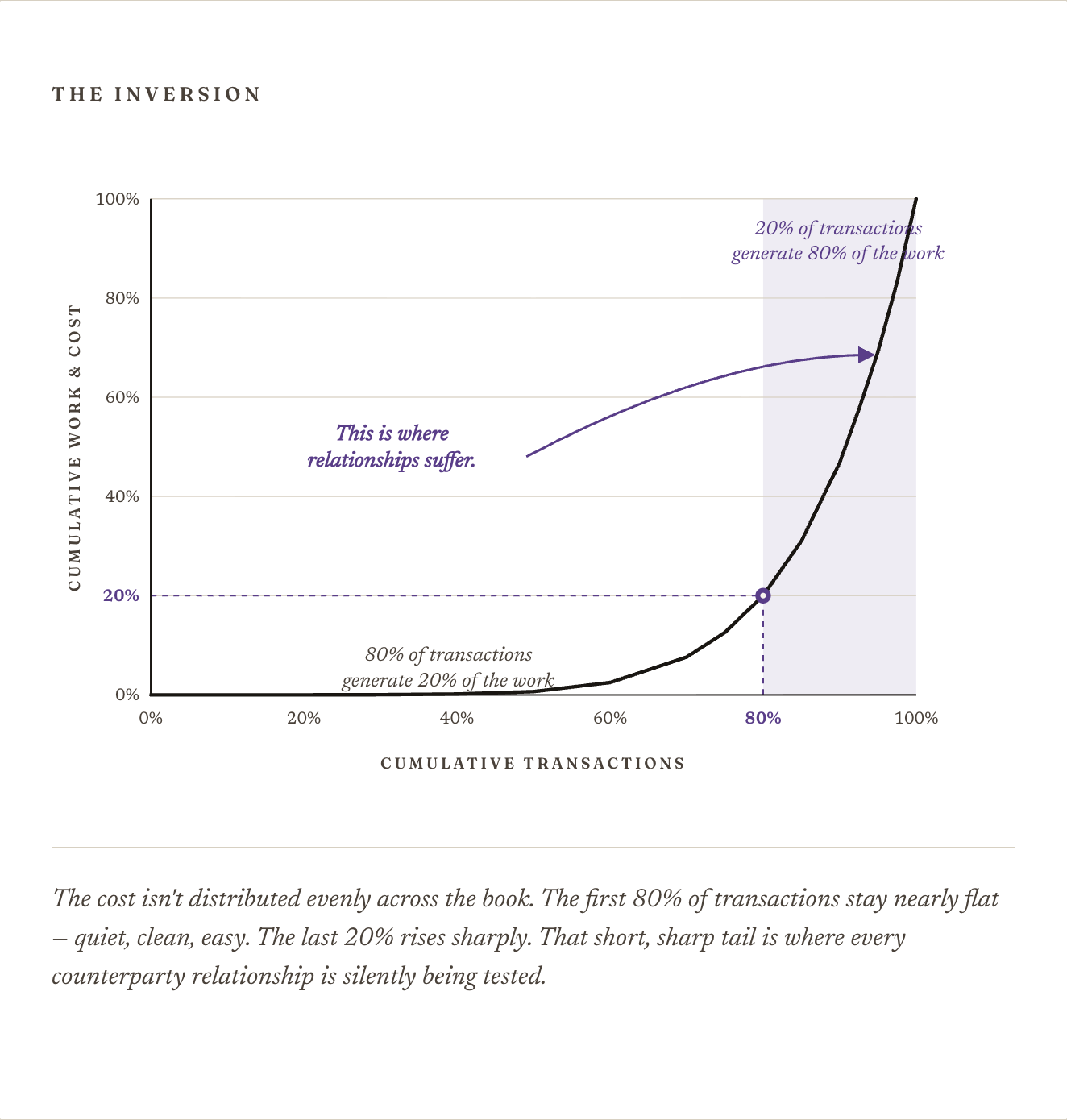

Eighty percent of insurance billing transactions run fine. Premium comes in. Money applies cleanly. Counterparties get paid. Nobody notices. That number is exactly why the rest of the work never gets done.

Every internal product team that has ever looked at the data has reached the same conclusion. Eighty percent is working. The remaining twenty percent is messy, idiosyncratic, expensive to engineer for, and low-margin to support. It goes to the bottom of the roadmap. Operations is told to handle it.

And operations does. Quietly. Year after year.

What gets missed in this calculation is the second half of the 80/20 rule — the half nobody quotes. The 20% of transactions that don't work consume 80% of the time, the headcount, the spreadsheets, the escalations, the late nights. That ratio inverts the entire economics of the function. And the roadmap, calmly, gets it backwards.

If the only consequence of the 20% were operational — more headcount, more hours, more software seats — the industry could rationalize it. Hire more people. Outsource. Build a marginally better spreadsheet. That has, in fact, been the plan.

The real damage is somewhere else.

It is relational.

Counterparties do not settle transaction by transaction. They settle on the book. That is the structural fact almost everyone in insurance technology underestimates.

A carrier doesn't open a ticket every time a single policy reconciles incorrectly. A premium finance partner doesn't escalate every individual return. They roll up. They net. They wait until the discrepancy is large enough — or persistent enough — to matter.

And then they call.

By the time that call happens, the conversation is no longer about a billing edge case. It is about a seven-figure number sitting in their reconciliation that doesn't match yours. It is about whether your numbers can be trusted. It is about whether the relationship can be operated at scale.

That call is expensive.

It pulls in your head of operations, your head of growth, your head of partnerships — and often the CEO. From there it trickles down into a multi-person, multi-week reconciliation effort: senior people pulled off their day jobs to chase a one-time problem that only exists because the 20% was never addressed.

The cost of the 20% rarely shows up where leaders are looking. It shows up downstream, in places that are hard to attribute back to a billing system:

None of this lives on the billing roadmap. None of it shows up in the product manager's analysis. It shows up in lost revenue, eroded leverage, and the slow, uncomfortable realization that the company has gotten harder to do business with.

The reason this hasn't been fixed — not by the AMS players, not by the policy administration vendors, not by the carriers themselves — is not that no one has tried. It is that from inside any single company, the problem doesn't look like a problem.

Every product manager runs the same analysis. Eighty percent running fine. A twenty percent tail that's expensive to engineer for and low-margin to support. The conclusion writes itself. The work gets pushed down. The operations team absorbs it. And the company runs comfortably on that arrangement until it gets large enough that a counterparty makes the call.

At which point it is no longer a billing problem.

Insurance professionals love to say this is a relationship business.

And then they stop saying it the moment back-office operations come up. Suddenly billing becomes "infrastructure." Reconciliation becomes "back-end." Cash application becomes a cost center. The work that holds the financial truth between every counterparty in the value chain — carrier, MGA, wholesaler, retailer, premium finance partner, insured — gets reframed as plumbing, and underinvested in accordingly.

The work of keeping the financial relationship clean between counterparties is not back-office work. It is the work. It is what determines whether the business can grow without losing the partnerships that make growth possible.

That reframing is the bug. Not a small one. The work of keeping the financial relationship clean between counterparties is not back-office work. It is the work that determines whether your business can grow without losing the partnerships that made growth possible in the first place.

Not by adding features to existing systems. Not by automating the transactions that already work. By building infrastructure that handles every billing model, every policy event, every counterparty, and every payment state as a first-class concern — so the seven-figure call doesn't happen, the relationship doesn't suffer, and the book stays clean.

Ready to replace tedious tasks with fast, accurate workflows? Book a free live demo of the #1 insurance financial operations platform today.

Functional FInance is a financial technology company, not a bank or FDIC-insured depository institution. Banking services are provided by Grasshopper Bank, N.A.; Member FDIC. The FDIC's deposit insurance coverage only protects against the failure of an FDIC-insured bank.